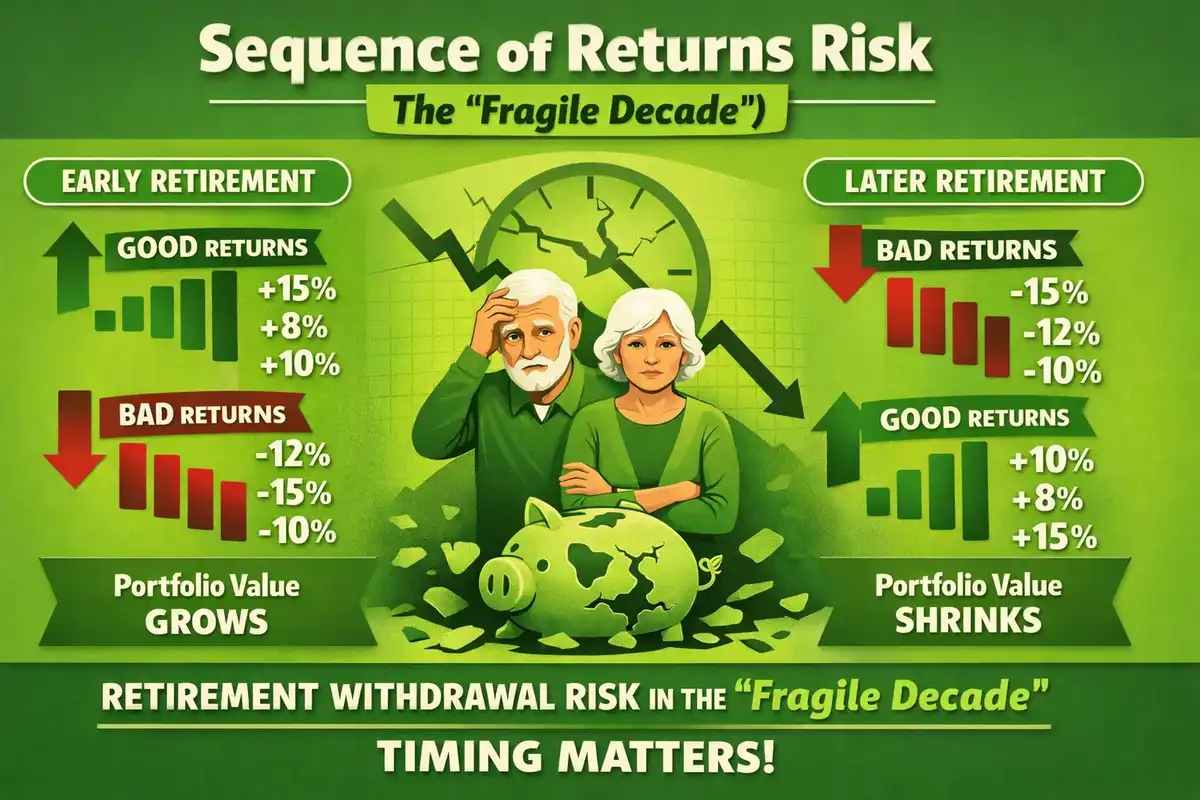

There is a risk in retirement that does not get nearly enough attention. It is called the sequence of returns risk. In simple terms, it is the danger of running into bad markets at the wrong time. If that happens in the early years of retirement, it can hurt your plan much more than if it happens later.

This risk shows up during what many in the planning world call the fragile decade. That is the five years leading up to retirement and the first five years after. In this article, you will learn what sequence of return risk means, the fragile decade, and how you can manage sequence of return risk.

What Is Sequence-Of-Returns Risk?

Sequence-of-returns risk, or sequence risk, is the risk that an investor will experience negative portfolio returns very late in their working lives and/or early in retirement. Wade Pfau retirement research demonstrates that returns during the first decade of retirement account for the lion’s share of retirement success.

Sequence-of-returns risk is a significant threat because retirees have little time to make up for losses that are compounded by the simultaneous drawdown of income distributions.

Understanding The Fragile Decade

The fragile decade refers to the five years before and five years after a person enters retirement. It is a transition period as a person shifts from accumulating wealth to living on savings and investments. The decisions a retiree makes during this decade will play a role in determining the lifestyle choices available to them throughout the remainder of their retirement.

How to Manage Sequence-of-Return Risk

Here are a few ideas to help retirees entering or nearing retirement manage sequence-of-return risk amidst market volatility.

-

Pad Your Reserves

Drawing down too much of your portfolio early in retirement can reduce its ability to generate income over time. To help mitigate this risk, retirees nearing the “fragile decade” may want to start building some short-term reserves.

Like preparing for a hurricane, those approaching retirement should be collecting and storing “supplies” to help them weather the storm. These reserves can help cover expenses early in retirement without requiring withdrawals from investments.

-

Manage Your Withdrawals

Some see withdrawals as a set amount over a period of time, whereas others anticipate managing withdrawals based on market conditions. A financial professional can help determine which approach may work best for you. Also, some may be able to reduce or skip withdrawals based on market conditions.

Historical research found that a constant, inflation-adjusted initial withdrawal of about 4% succeeded across most 30-year retirement windows. But others may not see that as a choice. With the guidance of a financial professional, investors can determine what fits their lifestyle.

You can even try the sequence of returns risk calculator to model different withdrawal scenarios and see how early losses affect income sustainability.

-

Consider Income Laddering

Laddering different types of retirement income is one approach that may help manage sequence-of-return risk.

A retiree buys fixed-income securities with different maturity dates so that they can quickly respond to changes in interest rates. A bond ladder helps manage reinvestment risk because the retiree owns a portfolio of fixed-income investments with varying maturities, allowing for reinvestment at prevailing market rates.

Some advisors combine a bond tent strategy with a bucket strategy retirement to protect near-term income while keeping long-term growth potential. These are simple and practical ways to reduce withdrawals during bad markets.

-

Gradually Transition into Retirement

No hard and fast rule says to stop working during retirement. On the contrary, many retirees find it beneficial to ease their way into full retirement. According to The Aging of America: A Changing Picture of Work and Retirement, in 2018, 9.1 million people reported still working either a full-time or part-time job past age 65.

Although many have initially prepared to stop working altogether, there are financial and personal benefits to maintaining a part-time job or encore career. Regarding sequence risk, continuing to work during a market downturn may allow you to manage the amount withdrawn from your investments.

-

Be Flexible and Thoughtful with Your Spending

You’ve likely spent years, decades even, preparing for retirement. So, the idea of “being flexible” may initially not make sense. But the markets are unpredictable, so managing your wealth can require adjustments and adaptability to new circumstances.

During the fragile decade, take the time to consider what your “must-haves” are and what you can feasibly live without. It may be helpful to prioritize your spending. Listing out expenses in order of importance can help you discern between what’s non-negotiable and what’s nice to have.

-

Delay Social Security Benefits

If you can address your retirement income needs without drawing down your investments, you may also want to consider delaying your Social Security benefits. The longer you wait to receive these benefits, the more you may receive per month.

Individuals are eligible to begin receiving Social Security benefits at age 62. However, you’ll receive a reduced amount if you take benefits before your full retirement age. On the other hand, you may be able to increase your Social Security benefits by taking advantage of delayed retirement credits.

Conclusion

The sequence-of-returns risk during the “fragile decade” can derail retirement plans, but it’s manageable. Build short-term reserves, use flexible withdrawal rules, consider income laddering, and use a sequence of returns risk calculator to test ideas. Small, practical steps and annual reviews with a financial professional can turn a fragile decade into a reliable, steady retirement income.

FAQs

What is sequence-of-returns risk?

It’s the danger of experiencing poor market returns right before or early into retirement, the “fragile decade.”

How can I protect my income early in retirement?

Build 2–5 years of liquid reserves, use income laddering or a bond tent/bucket approach, and test plans with a sequence of returns risk calculator to see how different scenarios affect withdrawals.

Should I delay Social Security?

Delaying Social Security can increase lifetime monthly benefits and reduce reliance on portfolio withdrawals. This is a useful tool if you can cover expenses another way early on.

Is working part-time helpful during market downturns?

Yes. Continuing part-time work or an encore role can reduce withdrawals, give breathing room during bad markets, and ease the fragile decade’s pressure.

How often should I review my retirement plan?

At least once a year and after major life or market changes. Regular reviews let you adjust withdrawal rules, reserves, and income ladders in time.