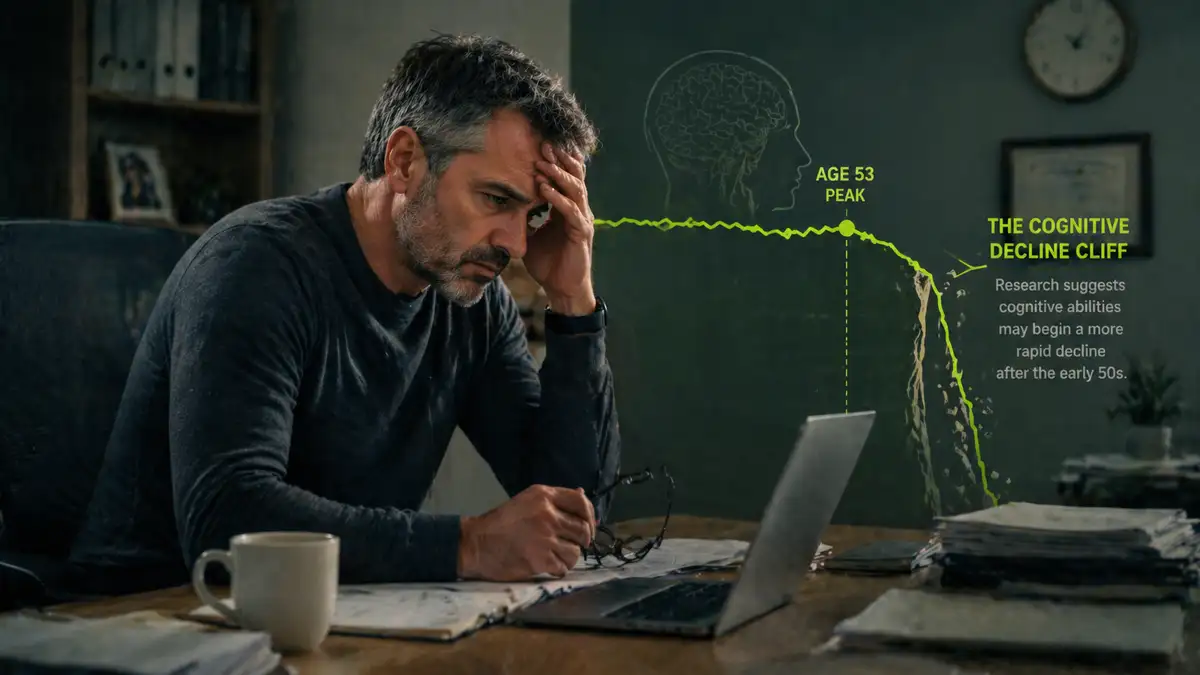

As your youth fades into the past, you might start to fear growing older. Studies find that people’s practical financial savvy follows an inverse-U-shape. It improves through early and midlife, peaks around the early to mid-50s, and then declines afterward. This is known as the cognitive decline cliff.

Longitudinal research also shows noticeable declines in cognitive test scores, followed by measurable reductions in household wealth. As older adults face cognitive decline, they are often a common target for scams and fraud. It is important for anyone with significant financial responsibilities to watch for early warning signs.

You will learn how cliffs affect everyday choices and how to take practical steps to maintain control and dignity.

What is Cognitive Decline Cliff?

The cognitive decline cliff is a pattern noticed by researchers. Some forms of learning and rapid problem-solving skills began to slow in the late 50s and early 60s. Other skills are also strengthened, such as experience and knowledge.

This explains why many older adults excel at recognizing familiar patterns or drawing on past experience. They struggle when faced with novel products or fast-moving digital systems. The brain becomes more selective, relying on what it already knows rather than adapting quickly to new information.

This shift directly affects cognitive decline financial decision making, especially when people are asked to compare new products or respond quickly to unfamiliar financial offers.

Are There Any Studies That Support Cognitive Decline Cliff?

Yes, there are some studies. Laboratory studies of perceptuo-motor learning show a marked drop in learning rates around the late 50s to 60s. At the same time, broader syntheses of many psychological traits indicate that overall mental functioning rises in the mid to late 50s.

Recognizing this mix is the first step towards sensible planning. As a result, people start simplifying portfolio for aging so that complex investments and scattered accounts can be managed without any mistakes.

Additionally, practical money choices depend on a fast blend of reasoning and the ability to weigh trade-offs under pressure. This blend is what the PBS reporting summarizes. It is noted that financial savvy tends to peak shortly after age 53.

Is There Any Age To Take Big Decisions?

There is no definite age at which you should not make any decisions. All these studies even support this and never mean important decisions should be avoided after this age. Instead, they highlight that the decision environment matters more. Complex choices benefit from written summaries and outside review rather than last-minute judgment calls.

After that point, people are more likely to make mistakes under stress or when choices are complex. This is not a moral failing but a predictable human pattern. The ability to spot this in yourself or your loved ones means you can change the process, not just the outcomes.

Some Practical Steps to Protect Your Money

The practical steps are straightforward and possible. You can protect your money in practical and respectful ways.

-

Design a clear legal plan

When someone is still able to make choices, design a power of attorney (POA) letter and sign it. This means you have trusted someone to handle your bills and bank accounts when you cannot.

Using a durable power of attorney finance structure ensures that authority continues even if mental capacity becomes limited. This way, you can protect both daily bills and long-term assets.

-

List your preferences and values

It is also helpful to explain your values and preferences in writing. A short letter describing how you want decisions handled can prevent confusion and conflict later, especially during stressful situations.

Add the name of the person who should be consulted for major buy and sales decisions, or someone who will look after the withdrawal and investment changes. Finally, review these key papers once a year and bring changes if you want.

-

Rules and regulations to avoid mistakes

Additionally, set some easy rules to avoid mistakes. Always ask for a second opinion on large withdrawals and provide the contact details of a trusted person at the bank. Update your list of accounts with passwords so the trusted person can easily access them.

These common steps prevent rushed decisions and make it harder for scammers or abusers to take advantage. They also support elder financial abuse prevention by adding delay and trusted oversight to transactions that might happen in isolation.

Conclusion

A good plan reduces complexity, adds oversight, and keeps dignity. You must simplify your accounts and documents so that anyone who is taking responsibility faces less confusion. You can share with your adult child or a trusted advisor the place where you have kept your documents, along with the statements and passwords. Consult advisers before you sell a business or move large sums of money. Even ask the institutions about hold or pause options when suspicious transactions appear. These practical steps limit exploitation and prevent mistakes caused by cognitive strain or isolation.

FAQs

What early warning signs reflect your cognitive decline?

When you miss paying bills and are confused about account matters. Or if you are asking the same question repeatedly, this warns you that you are getting old.

What steps can prevent you from bad money decisions?

Open your statements once a month, and write down decisions before you implement them. Always consider talking with an expert or a trusted person before you take a step.

What information must be shared with an adult child or a trusted person?

Tell them the location of your important papers and who to contact in an emergency.

When is the right time to set up a power of attorney?

The best time is before your decision-making skill weakens. Once you have savings, property, or business interests, choose a trusted person.

How can Financial scams be protected as age grows?

You should stay cautious with unfamiliar calls and investment offers. Double-check the information and never share personal details.